Introduction: Why Finding the Best Auto Loan Matters in 2024

Securing a low-interest auto loan is more crucial than ever in 2024, especially as car prices continue to rise. A low-interest rate can significantly reduce the overall cost of your vehicle, making monthly payments more manageable and saving you thousands over the life of the loan. When you lock in a good rate, you’re not just buying a car—you’re making a sound financial decision that impacts your budget for years to come.

The interest rate on your auto loan plays a pivotal role in the total cost of car ownership. Even a small difference in percentage points can translate into substantial savings or additional costs. For example, a loan with a 4% interest rate compared to a 6% rate on a $30,000 car could save you over $1,500 in interest payments alone over five years. That’s why it’s vital to compare offers and find the best rate available.

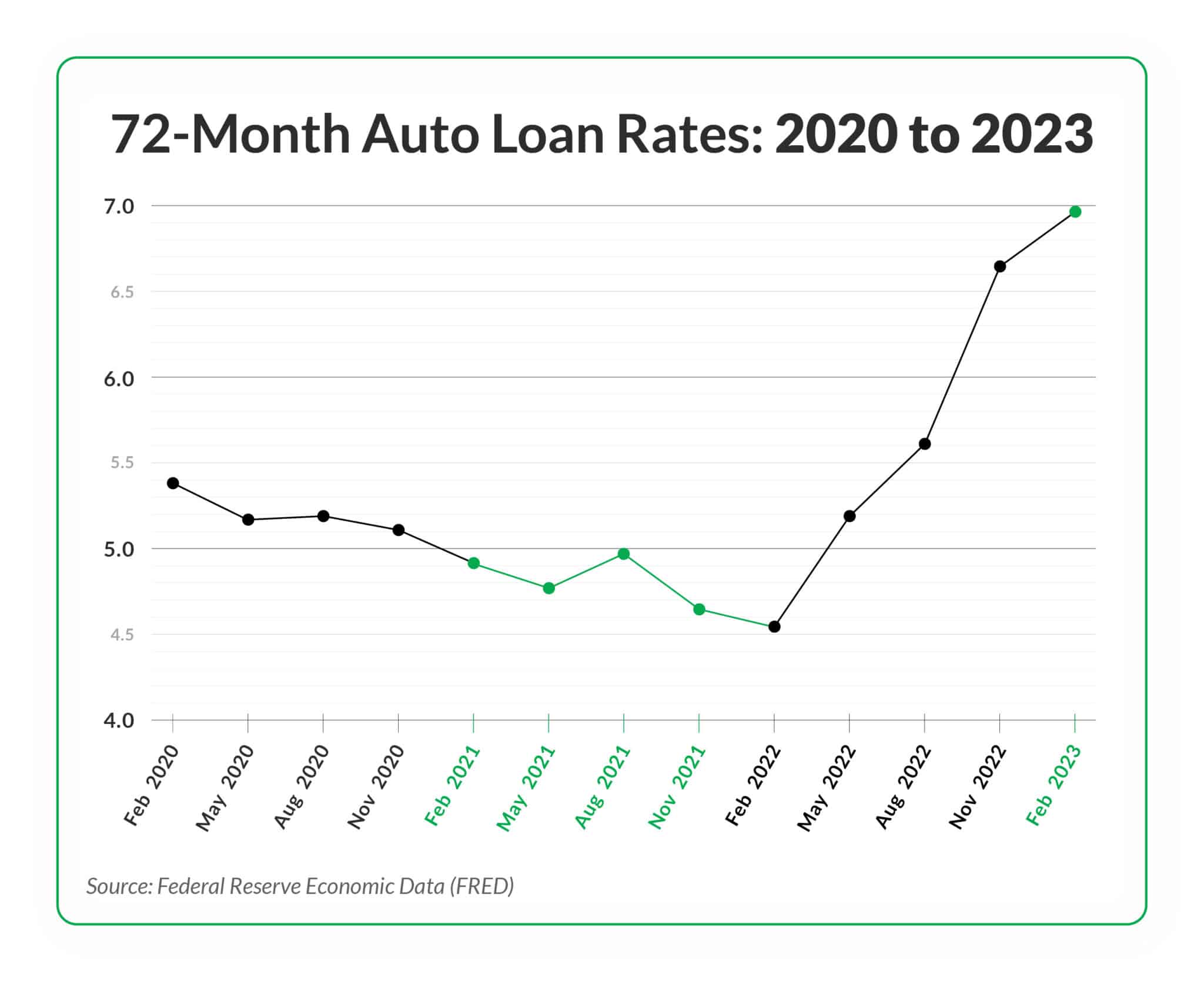

In 2024, several economic trends are influencing auto loan rates. With the Federal Reserve adjusting rates in response to inflation, the cost of borrowing has seen some fluctuation. Additionally, supply chain issues and changes in consumer demand are playing their part. Understanding these trends can help you time your loan application to secure the most favorable terms.

Current Economic Climate and Its Effect on Auto Loan Rates

The economic landscape of 2024 is shaping auto loan rates in several significant ways, making it essential for borrowers to stay informed. The interplay between inflation, Federal Reserve policies, and broader market trends is driving the cost of borrowing, directly impacting the rates you’ll encounter when seeking an auto loan.

Several key economic factors are currently influencing auto loan rates. Inflation continues to be a major concern, driving up prices across the board, including the cost of borrowing. As a response, the Federal Reserve has adjusted its policies, leading to fluctuations in interest rates. When the Fed raises rates to combat inflation, it becomes more expensive for lenders to borrow money, which in turn raises the interest rates they offer to consumers.

Federal Reserve policies are particularly impactful. In an effort to control inflation, the Fed may increase the federal funds rate, which directly influences auto loan rates. As the cost of borrowing rises for financial institutions, they pass on these higher costs to consumers in the form of higher interest rates on loans. This connection between Fed policies and loan rates is a crucial element for anyone looking to finance a vehicle in 2024.

Market trends are also playing a role in shaping auto loan rates. Supply chain disruptions and shifts in consumer demand, particularly in the automotive industry, are affecting vehicle availability and pricing. These factors contribute to the overall cost environment, influencing how lenders set their rates.

As we move through 2024, predictions for auto loan rates suggest continued volatility. Rates may fluctuate based on ongoing economic developments, such as further adjustments by the Federal Reserve or changes in inflationary pressures. However, staying informed and timing your loan application carefully can help you lock in a favorable rate despite these uncertainties. For those interested in understanding how these trends affect their financial decisions, keeping an eye on economic indicators and lender offers is essential to securing the best possible deal.

Top Banks and Credit Unions Offering Competitive Auto Loan Rates

When it comes to finding the best auto loan rates in 2024, certain banks and credit unions stand out for their competitive offers, favorable terms, and strong customer service. Understanding the differences between these lenders can help you make an informed decision and secure the best deal possible.

Top Banks with the Lowest Auto Loan Rates for 2024

- Bank of America: Known for competitive rates, often starting as low as 2.49% for qualified buyers. Bank of America offers flexible loan terms ranging from 12 to 75 months, allowing you to customize your payments according to your budget.

- Chase: Another leader in the industry, Chase is recognized for its exceptional customer service and a straightforward online application process, with rates starting around 2.49% for well-qualified applicants.

- Wells Fargo: Offers attractive rates, especially for customers with excellent credit scores, often in the 2.5% to 3.5% range. Wells Fargo also stands out for its quick approval process and the ability to manage your loan entirely online.

When comparing these banks, consider the terms they offer and the level of customer service provided. Each has its own strengths, so choose the one that best fits your needs and financial situation.

Credit Unions Offering Member Benefits and Special Offers

Credit unions are another excellent option for auto loans, often providing lower rates than traditional banks due to their non-profit status. Navy Federal Credit Union and PenFed Credit Union are two of the top contenders in 2024, with rates that can dip below 2.0% for well-qualified members.

Navy Federal Credit Union: Particularly popular among military members and their families, Navy Federal offers rates as low as 1.79% for new car loans and flexible terms up to 96 months.

PenFed Credit Union: Known for its easy membership requirements, PenFed allows virtually anyone to join and take advantage of their low rates and promotional offers.

In addition to competitive rates, credit unions often provide personalized customer service, making them a great choice if you value a more tailored banking experience. Their member-focused approach means you might also benefit from lower fees and better loan flexibility compared to traditional banks.

Online Lenders and Auto Loan Marketplaces: Finding the Best Deals

In the digital age, online lenders have become a popular choice for securing auto loans, often offering competitive rates and a streamlined application process. Additionally, auto loan marketplaces provide a valuable tool for comparing offers from multiple lenders in one place, helping you find the best deal with minimal effort.

Exploration of Online Lenders with Competitive Rates

Online lenders such as LightStream and Carvana have gained a reputation for offering some of the lowest auto loan rates available in 2024. LightStream, a division of SunTrust Bank, offers rates as low as 2.49% for borrowers with excellent credit, along with flexible loan terms ranging from 24 to 84 months. Their fully online application process is quick and straightforward, with same-day funding available in many cases.

Carvana, while primarily known as an online car retailer, also offers competitive financing options directly through their platform. They provide an all-in-one solution where you can shop for a vehicle and secure financing at the same time. Carvana’s rates start around 3.9%, and they offer the convenience of prequalification without affecting your credit score.

Another notable online lender is AutoPay, which specializes in refinancing auto loans but also offers new loans at competitive rates. AutoPay’s platform allows you to get prequalified offers from multiple lenders, giving you the ability to choose the best rate without impacting your credit score.

Benefits of Using Auto Loan Marketplaces to Compare Rates

Auto loan marketplaces, like LendingTree and AutoGravity, are powerful tools for borrowers looking to compare rates from various lenders. These platforms aggregate offers from multiple banks, credit unions, and online lenders, allowing you to see a range of options side by side. This can save you a significant amount of time and effort compared to applying with each lender individually.

LendingTree: Allows you to compare offers from up to five lenders in minutes. The platform also provides user reviews and ratings, helping you evaluate lenders based on other borrowers’ experiences.

AutoGravity: Particularly user-friendly, offering a mobile app that lets you shop for cars and financing simultaneously. This can be especially useful if you’re looking to streamline the entire car-buying process.

Tips for Navigating Online Platforms to Secure the Best Deal

To get the most out of online lenders and auto loan marketplaces, follow these tips:

- Prequalify When Possible: Look for lenders and marketplaces that offer prequalification without affecting your credit score. This allows you to compare rates risk-free before committing to a loan.

- Check for Fees and Penalties: Some online lenders may charge origination fees or prepayment penalties. Be sure to read the fine print and understand all associated costs before finalizing your loan.

- Read Reviews: Customer reviews can provide valuable insights into the lender’s reputation for service, transparency, and ease of use. Look for platforms like LendingTree that aggregate reviews to help you make an informed decision.

- Be Prepared with Documents: When applying online, having your financial documents, such as proof of income, identification, and vehicle information, ready can speed up the process and improve your chances of securing a favorable rate.

By leveraging online lenders and marketplaces, you can take control of the auto loan process, ensuring you get the best possible deal with minimal hassle. Whether you’re looking to finance a new car or refinance an existing loan, these platforms offer a convenient and often more affordable alternative to traditional banks.

How to Qualify for the Best Auto Loan Rates

Securing the best auto loan rates often comes down to preparation and understanding the factors that influence your eligibility. By focusing on your credit score, down payment, and the documentation needed for pre-approval, you can position yourself to receive the most favorable terms.

Credit Score Requirements and How to Improve Your Score Before Applying

Your credit score is one of the most critical factors lenders consider when determining your auto loan rate. Generally, a higher credit score translates into lower interest rates, as it signals to lenders that you’re a responsible borrower. In 2024, to qualify for the best rates, you typically need a credit score of 720 or higher. However, even if your score is lower, there are steps you can take to improve it before applying.

- Check Your Credit Report: Start by obtaining a copy of your credit report from major bureaus like Experian or Equifax. Review it for any errors or discrepancies that could be dragging down your score.

- Pay Down Debt: Reducing your overall debt, particularly credit card balances, can have a significant positive impact on your credit score. Aim to keep your credit utilization below 30% of your total available credit.

- Make Timely Payments: Consistently paying your bills on time is crucial. Even a single late payment can lower your credit score, so set up automatic payments or reminders to ensure you’re always on track.

Improving your credit score takes time, but even a modest increase can make a difference in the interest rate you’re offered.

Importance of a Down Payment and How It Affects Loan Rates

A down payment is another important factor that can influence your auto loan rate. The more you can put down upfront, the less risk you present to the lender, which often results in a lower interest rate. In 2024, it’s recommended to aim for a down payment of at least 20% of the vehicle’s purchase price.

- Lower Monthly Payments: A larger down payment reduces the total amount you need to borrow, which in turn lowers your monthly payments.

- Better Loan Terms: Lenders are more likely to offer favorable terms, including lower interest rates, when you reduce their risk with a substantial down payment.

- Improved Loan Approval Chances: A significant down payment can help you qualify for a loan, especially if your credit score is less than stellar. It shows the lender that you’re serious about your investment and financially stable.

Tips on Preparing Financial Documents and Getting Pre-Approved

Being well-prepared with your financial documents and getting pre-approved can give you a head start in securing the best auto loan rates.

- Gather Essential Documents: Lenders typically require proof of income (such as pay stubs or tax returns), proof of identity, proof of residence, and information about the vehicle you’re purchasing. Having these documents ready in advance can speed up the approval process.

- Get Pre-Approved: Pre-approval offers several advantages. It not only gives you a clear idea of the loan amount and rate you’re eligible for, but it also positions you as a serious buyer when negotiating with dealerships. Many lenders offer online pre-approval, which allows you to shop for cars with confidence, knowing your financing is already secured.

- Consider Your Budget: Before applying, carefully evaluate your budget to determine how much you can afford to borrow and repay. This includes considering all related costs like insurance, maintenance, and registration fees.

By focusing on your credit score, making a substantial down payment, and preparing the necessary documentation, you can greatly improve your chances of qualifying for the best auto loan rates available in 2024. Pre-approval is the final step that ties everything together, helping you approach the car-buying process with clarity and confidence.

Fixed vs. Variable Rate Auto Loans: Which Is Right for You?

When financing a vehicle, choosing between a fixed-rate and a variable-rate auto loan is one of the most important decisions you’ll make. Understanding the differences, benefits, and potential drawbacks of each option can help you select the loan type that best aligns with your financial goals, especially in 2024’s fluctuating economic environment.

Explanation of Fixed and Variable Rate Auto Loans

A fixed-rate auto loan has an interest rate that remains constant throughout the life of the loan. This means your monthly payments will stay the same, providing predictability and stability. Whether the market interest rates rise or fall, your rate is locked in from the start, allowing you to plan your budget with confidence.

On the other hand, a variable-rate auto loan (also known as an adjustable-rate loan) has an interest rate that can fluctuate over time, usually based on a benchmark interest rate, such as the prime rate. Initially, variable rates may be lower than fixed rates, but they can increase or decrease during the loan term, causing your monthly payments to vary.

Pros and Cons of Each Type in the Context of 2024’s Economic Environment

Fixed-Rate Auto Loans:

- Pros:

- Stability and Predictability: Fixed-rate loans provide peace of mind, knowing your payment amount won’t change, making it easier to manage your monthly budget.

- Protection Against Rate Hikes: With economic uncertainty and potential interest rate increases in 2024, a fixed rate shields you from the risk of higher payments if rates rise.

- Cons:

- Potentially Higher Initial Rate: Fixed-rate loans typically start with a slightly higher interest rate compared to variable-rate loans. In a declining rate environment, you might miss out on potential savings.

Variable-Rate Auto Loans:

- Pros:

- Lower Initial Rates: Variable-rate loans often start with lower interest rates than fixed-rate loans, which can save you money in the short term.

- Potential Savings if Rates Decrease: If interest rates fall, your loan payments could decrease, potentially lowering the total cost of the loan.

- Cons:

- Uncertainty and Risk: The primary downside of a variable-rate loan is the uncertainty. If interest rates rise, your monthly payments could increase, potentially straining your budget.

- Complexity: Variable-rate loans can be more complicated to understand, requiring careful monitoring of market conditions to avoid surprises.

Guidance on Choosing the Best Option for Your Financial Situation

Deciding between a fixed and variable rate auto loan depends largely on your financial situation, risk tolerance, and expectations for the future.

- Choose a Fixed-Rate Loan If:

- You prefer stability and want to know exactly what your monthly payments will be for the duration of the loan.

- You believe interest rates are likely to rise and want to lock in a rate now to avoid higher payments later.

- You have a tight budget and can’t afford the risk of fluctuating payments.

- Choose a Variable-Rate Loan If:

- You’re comfortable with some level of risk and are willing to gamble on the possibility of lower payments if rates decrease.

- You expect to pay off the loan quickly, before significant rate changes could impact your payments.

- You have flexibility in your budget to accommodate potential increases in your monthly payment.

In 2024, with the economic environment being somewhat unpredictable, many borrowers might lean towards the security of a fixed-rate loan, particularly if interest rates are expected to rise. However, if you’re confident that rates will remain stable or decline, and you have the financial flexibility to handle potential rate increases, a variable-rate loan could offer initial savings. Ultimately, the best choice is one that aligns with your financial goals and offers peace of mind as you navigate the car-buying process.